There Are No Free Products

Free products aren't truly free. The costs are just not obvious.

In the summer of 2017, Albert ran out of cash. At the time, Albert had 50,000 devoted users who used the app to budget and save. But Albert was free, and we lost money every month.

Free was the status quo for new financial apps. CreditKarma pioneered the model with free credit scores. Robinhood followed with free trading. Our original plan at Albert was to follow this model. After a successful seed investment round based on this pitch, we soon realized that while CreditKarma could make money by referring users to credit cards and Robinhood could make money by taking a small cut from every trade, there was no equivalent in personal financial management.

Money management apps must give objective, impartial advice, and you can't trust a financial management tool that gets paid for every financial product it pushes.

Our initial strategy almost proved fatal.

August 11, 2017

In early August 2017, after one last unsuccessful fundraising attempt, we had one option left: ask customers to pay.

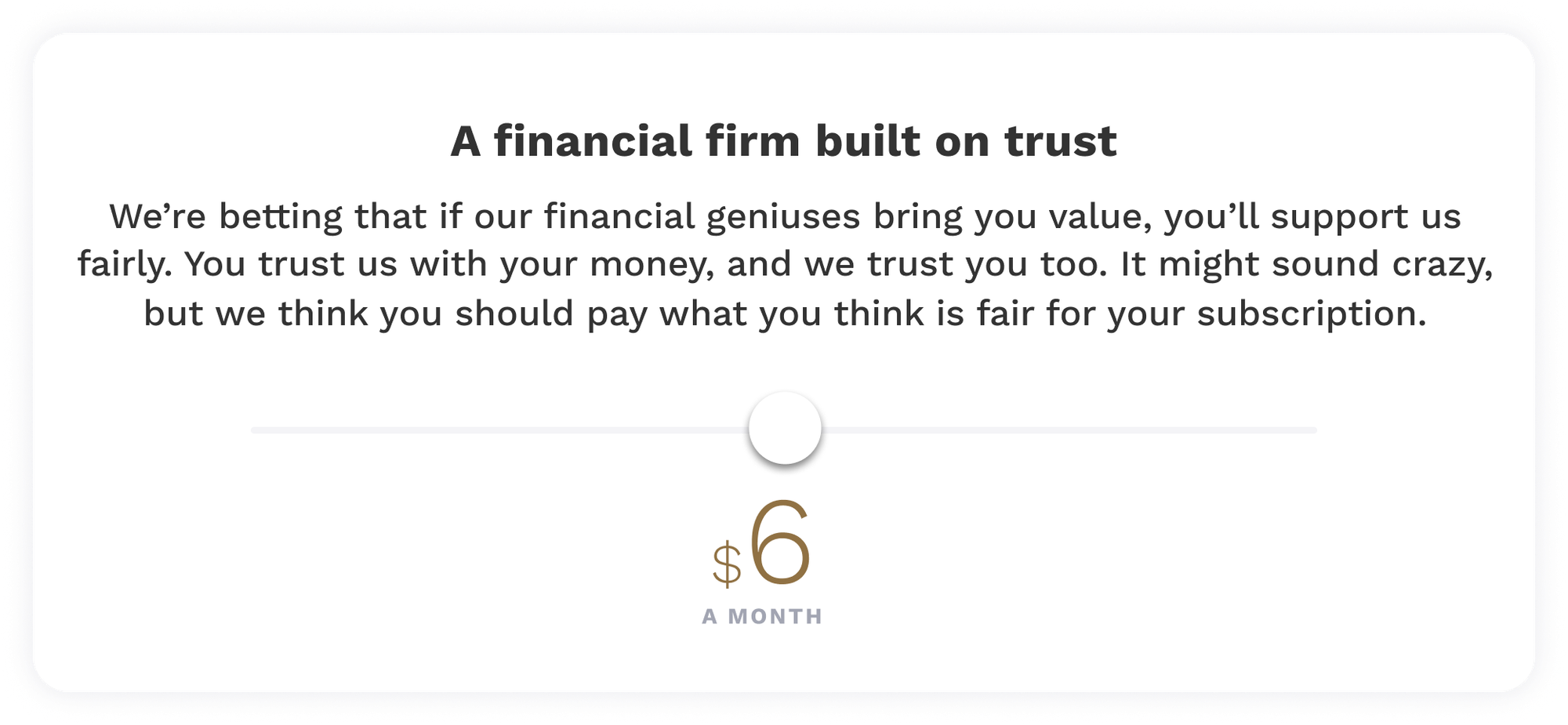

We needed to be sure that customers loved the product enough to pay for it long-term, so we asked every user to pay what they thought was fair. We showed a slider ranging from $0 to $14 a month, and the user could pick any value. Below is the original screen from the app.

Albert's original pay what's fair screen

On the morning of August 11, 2017, we launched the slider above. Over half of our users voluntarily chose to pay more than $0, averaging $4 per month. Albert went from $0 to $1 million in annual recurring revenue almost overnight.

We had almost missed the most obvious way to build a sustainable business: charging the customer. Over the ensuing five years, fintech companies mostly followed.

Product | Company | Monthly fee |

Automated investing | Betterment | $4/month or 0.25% of assets |

Automated investing | Stash | $3/month for basic plan; $9/month for full plan |

Automated investing | Acorns | $3/month for basic plan; $5/month for full plan |

Banking for families | Acorns | $9/month for teen banking |

Financial advice | Betterment | 0.40% of assets annually, $20k in minimum assets |

Financial advice | Fruitful | $98/month |

Identity monitoring | Lifelock | $11.99/month for basic plan; $34.99/month for mid plan. Discounts for paying annually; prices go up in year 2. |

Maintenance fee | Bank of America | $4.95/month if you keep <$500 balance |

Maintenance fee | Chase | $12/month unless you switch direct deposit to Chase or maintain $1,500/month on average |

Overdrafts | Chase | $34 per overdraft |

Overdrafts | Wells Fargo | $35 per overdraft |

Personal financial management | Copilot | $13/month, $7.92/month paid annually |

Personal financial management | YNAB | $14.99/month, $8.25/month paid annually |

Financial features and products that charge customers as of December, 2023.

Customers pay for things they use

Charging customers aligns incentives and promotes a healthy business with no hidden costs.

Some loud customers will tell you that your product should be free. Investors may tell you that your product should be free to promote growth. Who doesn't like free stuff?