The Formula for a Successful Financial Product

A simple formula for building a consumer product: get users, build multiple products, run efficiently.

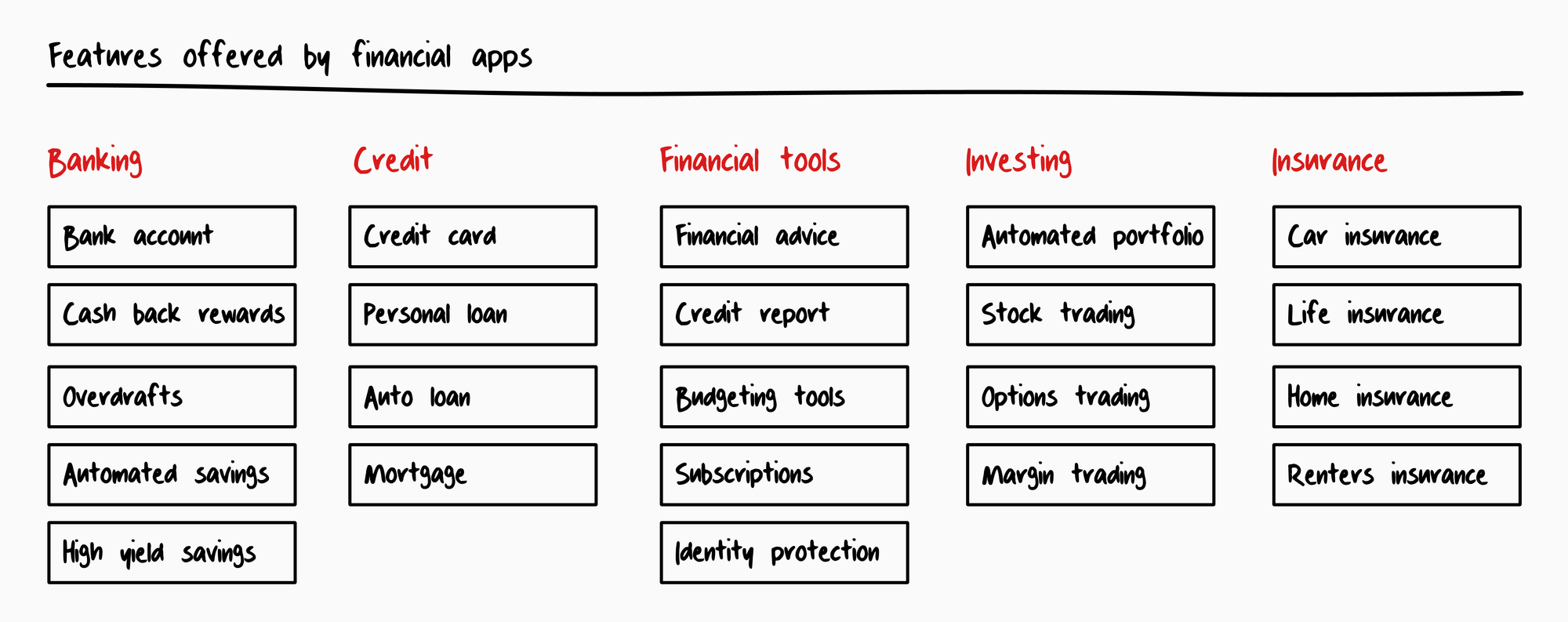

Over the past two decades, financial apps have tried to take market share from large financial institutions. While a handful of new financial companies have reached scale, most have failed, leaving a scrapyard of defunct banking, saving, investing, lending, insurance, discounts, payments, and budgeting apps.

Investors are now largely convinced that building a successful consumer financial product is near impossible. But this is wrong. There is a formula for success that took me nearly a decade of building Albert, the banking app I run, to understand.

The challenge

There are three primary challenges to building a successful consumer financial product:

- Prioritization. There are dozens of financial products for a company to choose from. It's tempting to build everything. Unchecked, this leads to lack of focus. Companies must prioritize the right features.

- Time to ship. A new company can build one financial product before running out of money, because each financial product takes at least a year to launch. Pivoting from, say, a bank account to a loan requires more capital and another year of work. Again, companies must prioritize the right features.

- A single product is not enough. In contrast to most software businesses (e.g. accounting software), consumer financial companies need multiple core products to truly succeed. This is true for every large, profitable financial institution in America.

Companies who build the wrong features early usually fail. Financial companies that never make it past a single product don't achieve their full potential.

High yield savings seems like an obvious product to build today because everyone should want to earn 5% on their savings.

At Albert, we focus on customers making less than $100k a year, with a median annual income around $50k (the majority of Americans under the age of 40). On average, financially responsible customers earning $50k/year save $500 a year after retirement contributions. 5% of $500 saved is $25. 3 years of savings is $1,500, earning $75 of interest a year (non-retirement savings generally don't build up for more than several years).

In contrast, offering 2% cash back on our customer's $2,000/month of credit or debit card spend is $480 a year in savings. A great cash back program can offer more than 5x the value of a high yield savings account!

Of course, this doesn't mean that high yield savings accounts shouldn't be built for most Americans. $75 is valuable. It only means that a startup serving the broad American consumer should build other things that offer more value first.

Three steps to success

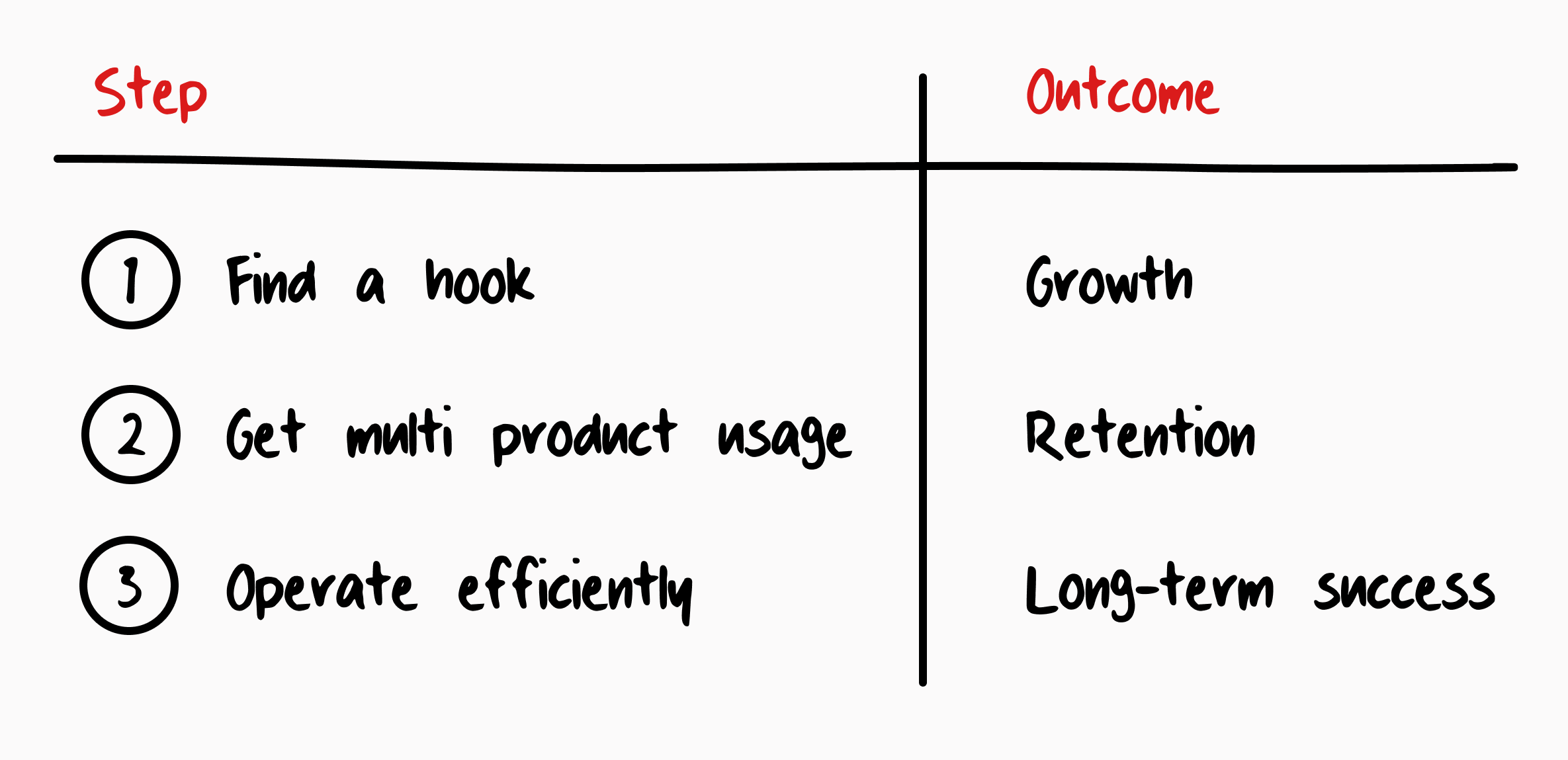

There's a simple formula for building a successful consumer financial product.

With the right design and engineering talent, operational skill, and focused leadership, any financial company can succeed by following three steps: