From High Cash Burn to Profit: How to Transform a Company

When venture capital dried up in early 2022, companies began charting a new path. The outcome: profit.

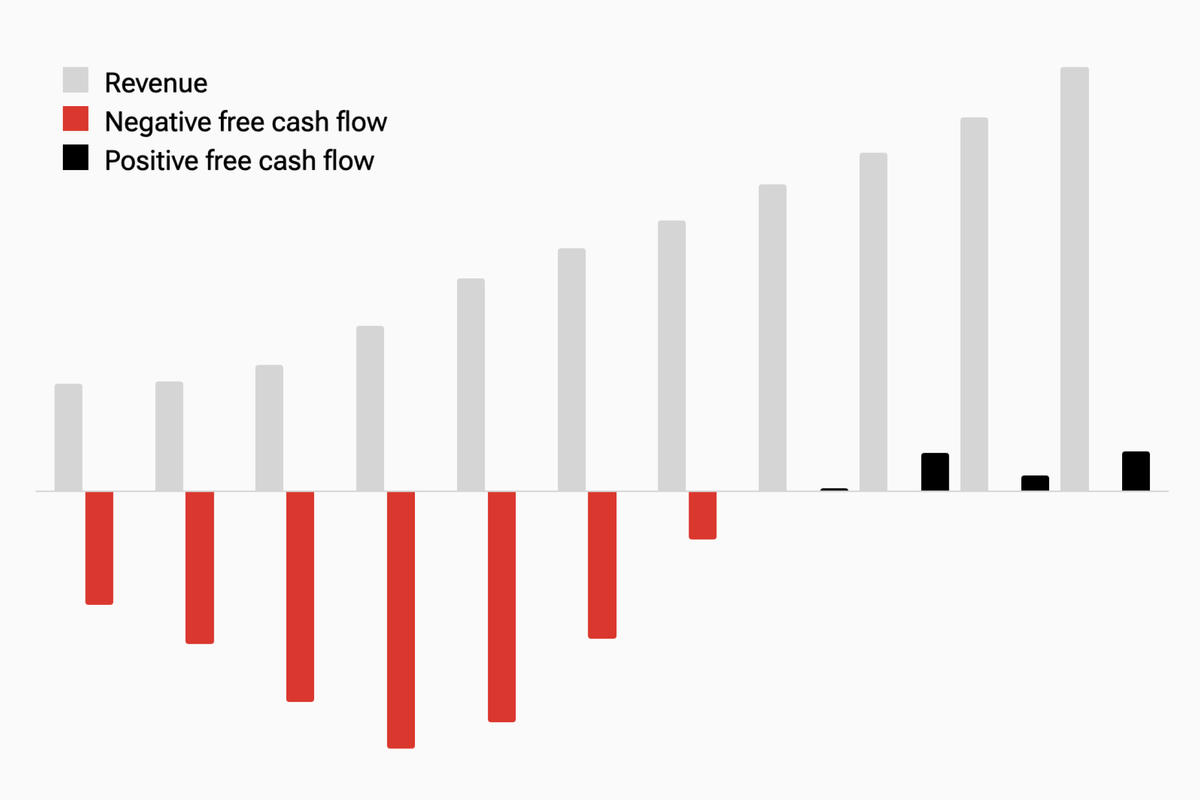

In January 2022, I tried to raise money for Albert, the company I run. The business was doing well, generating $75 million of annualized run-rate revenue.

I had raised $200 million over the company's first six years, but this time was different. Albert was burning millions of dollars a month, and investors had suddenly lost appetite for funding an operating loss. Growth-at-all-costs, tech's calling for nearly a decade, was about to fall out of favor, but most companies had no idea because they were not actively fundraising.

This post is the first in a series of posts on how to transform a fast-growing, money-losing company into a profitable one, without sacrificing growth.

The macro environment

Here's what I wrote in early 2022 to Albert's leadership team about the environment:

I have spent the last several months meeting with investors, and the market is undergoing a substantial shift. The appetite for investing in unprofitable businesses is gone, and we must adapt.

The macro-economic environment is changing. Inflation has spiked because the Fed printed a lot of money. The Fed must now raise interest rates to curb spending. This has cooled public and private investment, and it will also likely lead to a recession. In times of uncertainty, investors look for safety. As a result, most high growth public stocks are down 75%+ from their highs, and mid/late stage private investment, starting at Series B, is paused.

The past 15 years of consumer fintech can be divided into 3 phases:

1. Users: from 2008-2015, companies like Mint gained millions of users. This was a watershed moment, because it proved mass adoption of new tech-driven financial products.

2. Monetization: starting in 2015, investors looked past eyeballs to measure success and shifted focus to revenue. From 2015-2021, consumer fintech figured out revenue: subscription, interchange fees, referral fees, payment for order flow, money movement fees, and more. Albert has been one of the successful fintech companies in both the user and monetization phases.

3. Profitability: investors are now looking for the subset of these businesses which will become profitable. This simply means that revenue > all spending, no different from our personal budgets. Today, most consumer fintech companies are not profitable: Robinhood, Affirm, Sofi, Chime, NuBank, Varo, Current, Dave, and Albert.

If you can earn 5% risk free by lending to the U.S. government, and public companies are trading at historically cheap multiples, why invest in an illiquid, late stage private company that could go bankrupt because it's losing money, only to earn 15-20%? This quickly becomes a self perpetuating cycle: less private investment drives more private investors away because there is no liquidity. And tech companies, who for decades lost money to reach scale, suddenly find themselves without capital to survive.

Changing course

Here's the rest of the letter I sent to management, dated early 2022: